The basics of the Marketplace Health Plans

The “ins and outs” of the Marketplace plans made available by the Patient Protection and Affordable Care Act PPACA can be very confusing to understand. For some the Marketplace Health Plans are their best option, but not so for others. It can be very confusing to navigate all of the information out there about the Marketplace, decipher the jargon and determine what information is reliable and what is not.

Here are some basics of the Marketplace Health Plans that may assist you:

- The Marketplace insurance plans were made available when the Patient Protection and Affordable Care Act (PPACA) was written into law on March 23, 2010. The PPACA is also known as Health Care Reform, Affordable Care Act and Obamacare.

- Marketplace insurance plans are available through marketplace exchanges specific to each state which can all be accessed through the government’s health care website.

- Traditionally, you can only enroll in these plans during open enrollment. Open enrollment for 2016 coverage is November 1, 2015 – January 31, 2016. Coverage with these plans will begin on January 1, 2016.

- Outside of open enrollment you can only enroll in these plans if you qualify for special enrollment. Special enrollment is usually available as a result of a life changing event such as marriage, birth of a child or loss of current coverage. Read More About Special Enrollment

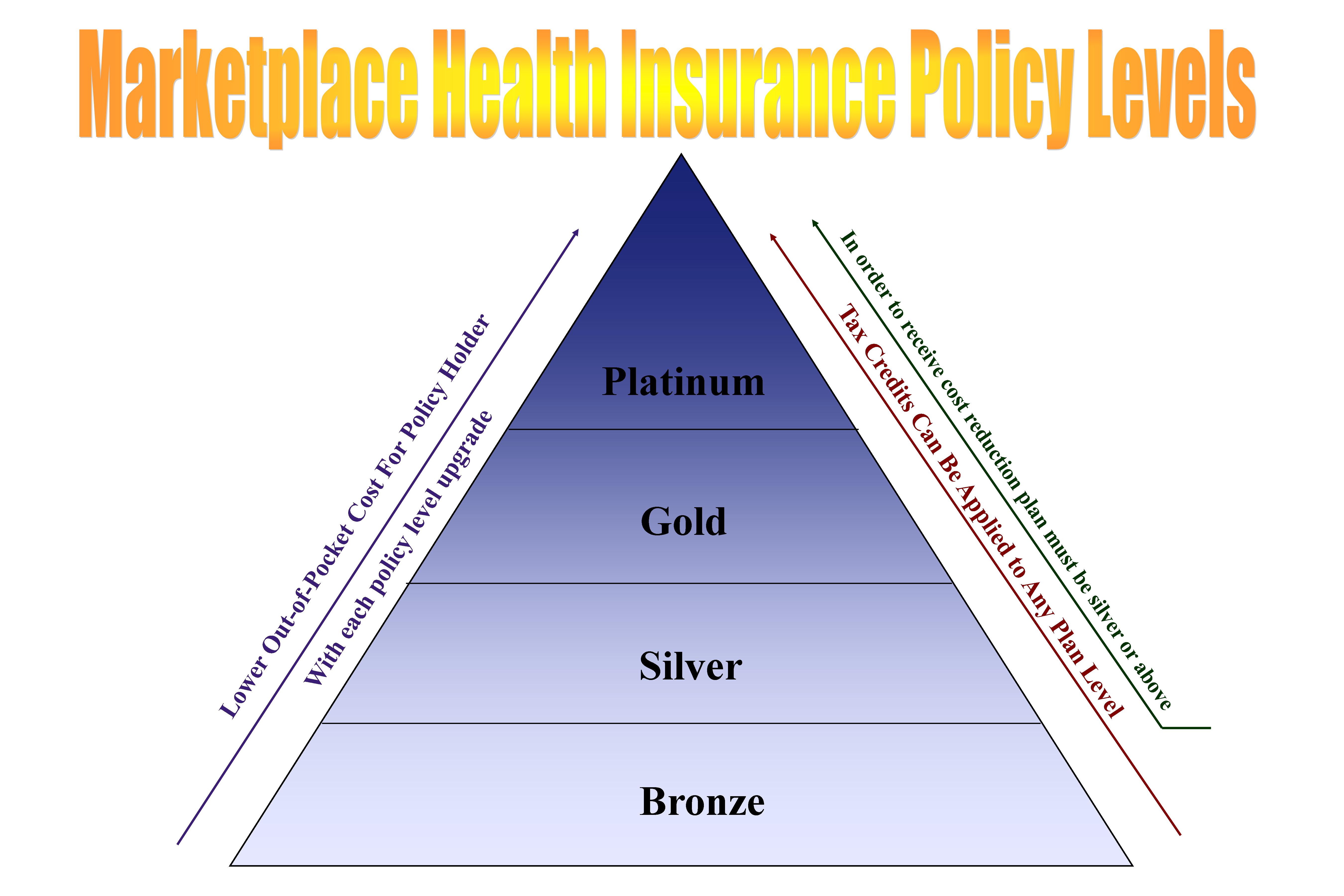

The Marketplace Health Plans are available in four different coverage levels: Bronze, Silver, Gold and Platinum. Bronze is the most affordable plan level with the lowest premiums and higher out-of-pocket costs. With each subsequent plan level there are fewer out-of-pocket costs with higher monthly premiums.

The Marketplace Health Plans are available in four different coverage levels: Bronze, Silver, Gold and Platinum. Bronze is the most affordable plan level with the lowest premiums and higher out-of-pocket costs. With each subsequent plan level there are fewer out-of-pocket costs with higher monthly premiums.

(click to view chart)

There is financial assistance available to help make coverage more affordable for those who qualify. A person or family’s household income is evaluated in order to determine if they qualify for assistance. There are two types of financial assistance that can be applied to Marketplace health plans: premium tax credit or cost sharing subsidy.

- Premium tax credit: is an advance-able tax credit paid by the IRS (Internal Revenue Service) to the insurance carrier to offset the cost of a policy’s premium.

- Cost Sharing Subsidy: reduces the out-of-pocket cost, such as deductibles, copays and coinsurance, that the policy holder may be responsible for. This is reserved for the lowest-inclome Marketplace enrollees.

If available, the tax credit can be applied to any of the four health plan levels. However, to apply a cost sharing subsidy to a Marketplace Health Plan a silver level plan or above must be chosen.

For more information or to get some quotes on a Marketplace Health Plans give us a call today! Our knowledgeable agents are very experienced with the Marketplace health plans and how to ensure you receive the appropriate financial assistance should you qualify! Fill out this request form and lets get you the coverage you need for a price you can afford!

*Due to changes in the insurance industry as a result of Affordable Care Act regulation IHS Insurance Group is no longer able to offer Marketplace Health Plans. Please see our “Resources” tab and click the link to the healthcare.gov website if you care to apply.

E. Steele